Life Insurance Basics: Life Insurance Pricing and Policy Mechanics

By Ryan Barradas

Originally posted May 2015; Revised August 2022

The pricing of life insurance policies is complex and dynamic. There are four factors that primarily drive pricing and policy performance: mortality, investment earnings, expenses and taxes, and persistency. The impact of the varying pricing factors on life insurance policy performance will vary in importance depending on the type of policy design. Each pricing factor is based on current experience, usually from the insurer itself but sometimes complemented by data from actuarial consulting firms, public sources, or reinsurers.

Life Insurance Policy Pricing Factors

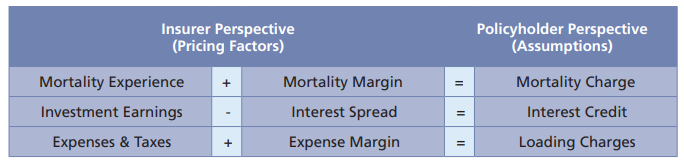

Life insurance products are based on a few key pricing factors that affect the cost of the life insurance policy and its future policy performance. For an insurance carrier, these can be summarized in three pricing factor categories: mortality, investment performance and internal costs. Mortality involves how many insureds pass away on an annual basis and how much capital needs to be paid out by the carrier in the form of a death benefit. Investment performance involves how well the carrier’s investments have performed in the capital markets and what costs were incurred to make those investments. Lastly, the carrier has its own internal costs to run its business, such as staff, technology, and other operating expenses. These three categories affect the policyholder in the form or charges or credits on their life insurance policy.

Mortality Charge

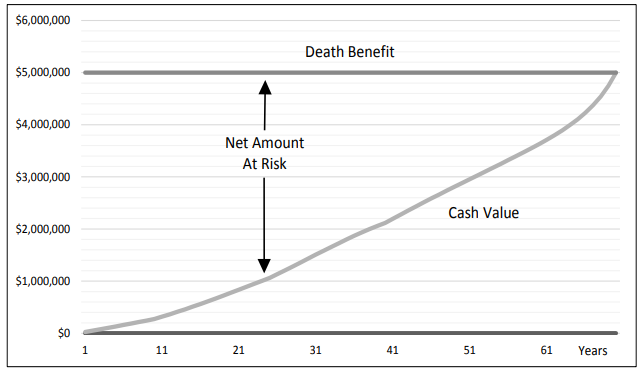

A mortality charge is a policy charge intended to cover the death claims paid by the insurance company. Mortality charges are primarily based on insurance company’s recent historical mortality experience. Two of the most common types of insurance products are Universal Life and Whole Life. Universal Life products are a permanent type of insurance where the policyowner invests in the general account of the insurance carrier. For Universal Life, the mortality charge is transparent (i.e., unbundled) and defined as the cost of insurance (COI) charge. Whole Life, also known as traditional life insurance, is another type of permanent life insurance. However, it is more restrictive than Universal Life and requires guaranteed premiums which generates a guaranteed cash value and death benefit. For Whole Life, the mortality charge is not explicitly revealed, but is included in the guaranteed values and dividends (i.e., bundled). Specifically for Universal Life, the COI charge is a function of a COI rate multiplied by the net amount at risk (NAR). The COI rate is equal to the probability of death and loaded for deviation contingencies, profit, and potentially to cover other insurer expenses. The NAR equals the total death benefit less the cash value. Consequently, mortality charges will be higher for lower premium funding due to the lower resulting account values (and higher NAR) and vice versa. See illustrated NAR example below.

Interest Credit

A Universal Life insurance policy provides a crediting interest rate applied to the underlying cash value. Whole Life insurance policies provide a dividend interest rate not applied to the underlying cash value but bundled within the dividend. Both rates are subject to guaranteed minimums and are typically backed by the issuing insurance company’s portfolio of high-quality fixed income instruments such as bonds and mortgages. Variable contracts are different in that their credited investment earnings are based on sub-account allocations, which may include investment options, such as equities and fixed income, chosen by the policyholder and are not subject to a guaranteed minimum (i.e., 100% of the investment risk is transferred to the policyholder). Index UL contracts credit interest based on the gain of an underlying index (e.g., S&P 500) and subject to a participation rate (e.g., 100%), cap rate (e.g., 12%), and floor (e.g., 0%).

Loading Charges

Loading charges are policy charges intended to cover insurer expenses, taxes, and contingencies; for Universal Life loading charges can come in a variety of forms:

• A flat dollar amount assessed per month

• A percentage of premium charge

• A charge per $1,000 of face amount

• And sometimes an asset-based fee (percentage of account value)

For Whole Life insurance policies, the loading charges are bundled in the guaranteed values and dividends and are usually not transparent, but they are certainly being applied.

Surrender Charge

Some policies include an additional charge assessed against a policy’s cash value and only applied if the policy is terminated early (i.e., surrendered).

Persistency

Persistency is another pricing factor that typically is not disclosed whether the product is bundled or not. Persistency reflects the ratio of policies that stay in force (i.e., do not lapse or are not surrendered). Typically, strong persistency helps policy pricing and performance as it supports ongoing insurer earnings from the policies remaining on the books.

In both unbundled and bundled policies, the insurer uses the policyholder charges to cover death claims and expenses, and credits interest to the policy based on investment earnings. The margins and spreads are incorporated by the insurer to provide contingencies for deviations in experience and provide profit. The entire package of loadings and credits determines insurer profitability and policy performance.

Life Insurance Policy Mechanics

Some life insurance products, such as Universal Life, are unbundled where the interest credits and charges are transparent and represent current insurer experience. The underlying policy contract specifies the individual credits and charges and most carrier illustration systems can provide specific details.

Other products, such as Whole Life, are bundled where the interest credits and charges are not transparent, but all the pricing factors still apply. For Whole Life, the dividend represents a bundled credit for current experience that is more favorable than other conservative guaranteed factors. The individual components impacting the dividend are not reported.

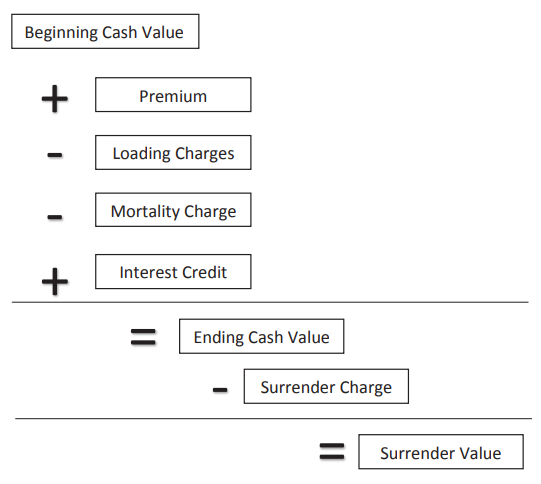

For Universal Life, which has flexible premiums, policy coverage remains in force as long as the cash value remains positive (the policy lapses when the cash value goes to zero). For Whole Life, the fixed premium schedule ensures a positive cash value for life. For both policy types, the cash value is simply an accumulation of premium (policy owner payment made to an insurance company to place and maintain an insurance contract in effect), interest credits, and loading charges (refer to chart below). Some policies include a surrender charge that only applies if a policy is fully surrendered.

Summary

Life insurance pricing components can be, and are, mixed in different ways (i.e., product designs) by insurers to accomplish different marketing and profit objectives. The precise mix will be driven by the competing interests of policy performance and profitability, coupled with the insurer’s underlying mortality, investment, expense, and persistency experience. Strong results in each category can lead to positive life insurance policy performance and lower overall charges.