Repurposed PPLI: A Smarter Way to Unlock More from Existing Life Insurance

Published: February 19, 2026

Many affluent families already hold significant life insurance policies in place for estate planning. Those policies were thoughtfully designed, properly funded, and intended to serve a long-term purpose. But over time, portfolios grow, tax exposure increases, and investment opportunities expand. The question becomes: is the existing structure still doing as much as it could?

Repurposed Private Placement Life Insurance (PPLI) offers a way to build on what is already in place. It transforms an existing life insurance policy into a new PPLI policy—without losing any current benefits. Instead of replacing coverage or restarting underwriting, Repurposed PPLI allows families to maintain their existing death benefit while adding a tax-advantaged investment component designed to grow alongside it.

The result is not a new strategy. It’s a more efficient structure.

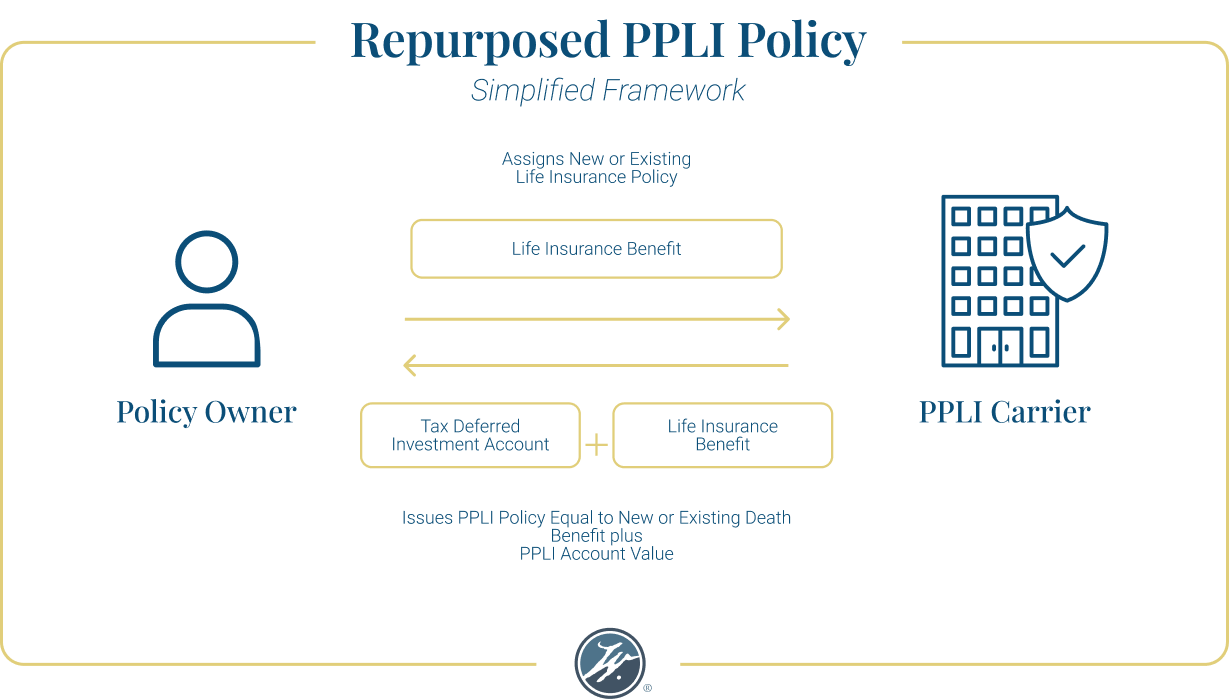

What Is Repurposed PPLI?

Repurposed PPLI takes an existing life insurance policy and converts it into a new Private Placement Life Insurance structure while preserving the original death benefit.

This approach delivers three core advantages:

- No medical underwriting. No exam. No medical records. No lengthy implementation timeline

- Existing coverage remains intact. The original death benefit stays fully in place

- A tax-advantaged investment account is added. Assets grow tax-deferred and can be accessed tax-free. Beneficiaries receive both the investment account and the death benefit tax free

For families already carrying permanent life insurance, this structure doesn’t require undoing prior planning decisions. It builds on them.

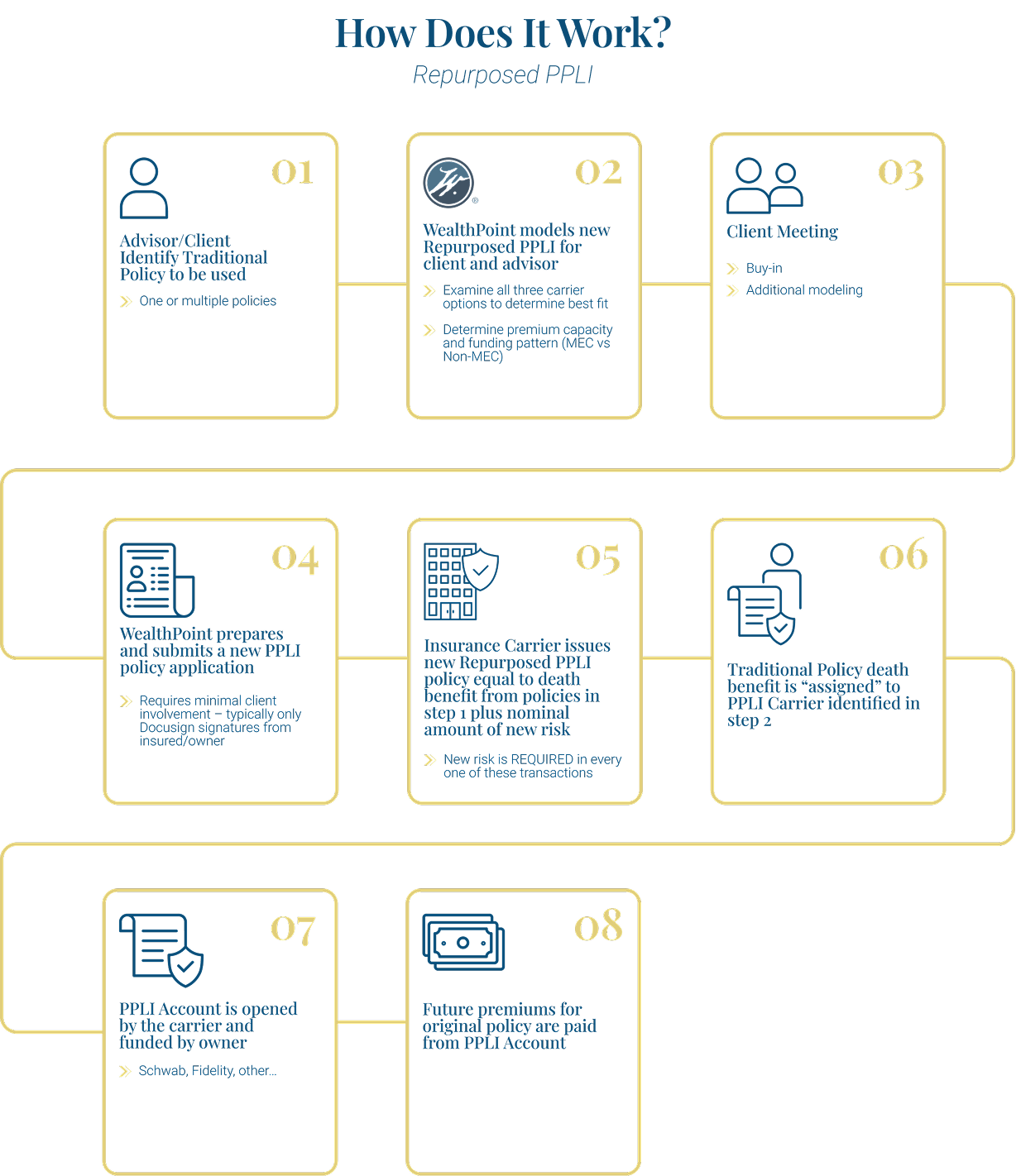

How Repurposed PPLI Works

At its core, the structure is straightforward. A new PPLI policy is secured by assigning the existing death benefit to a PPLI carrier. The new policy’s death benefit equals:

Existing policy death benefit + PPLI investment account + growth

This is not an incremental change. It meaningfully reshapes how wealth compounds inside the policy.

Here’s a hypothetical example

- Male, age 60

- Existing $20 million policy in place for estate planning

- Investment return assumption: 8%

- Average effective tax rate: 32.3%

A practical rule of thumb applies: the insured’s age is approximately equal to the percentage of the death benefit that may be contributed as new PPLI premium, slightly lower for second-to-die policies. In the example provided, the maximum premium contribution was $12 million.

What happens when that structure is modeled over time?

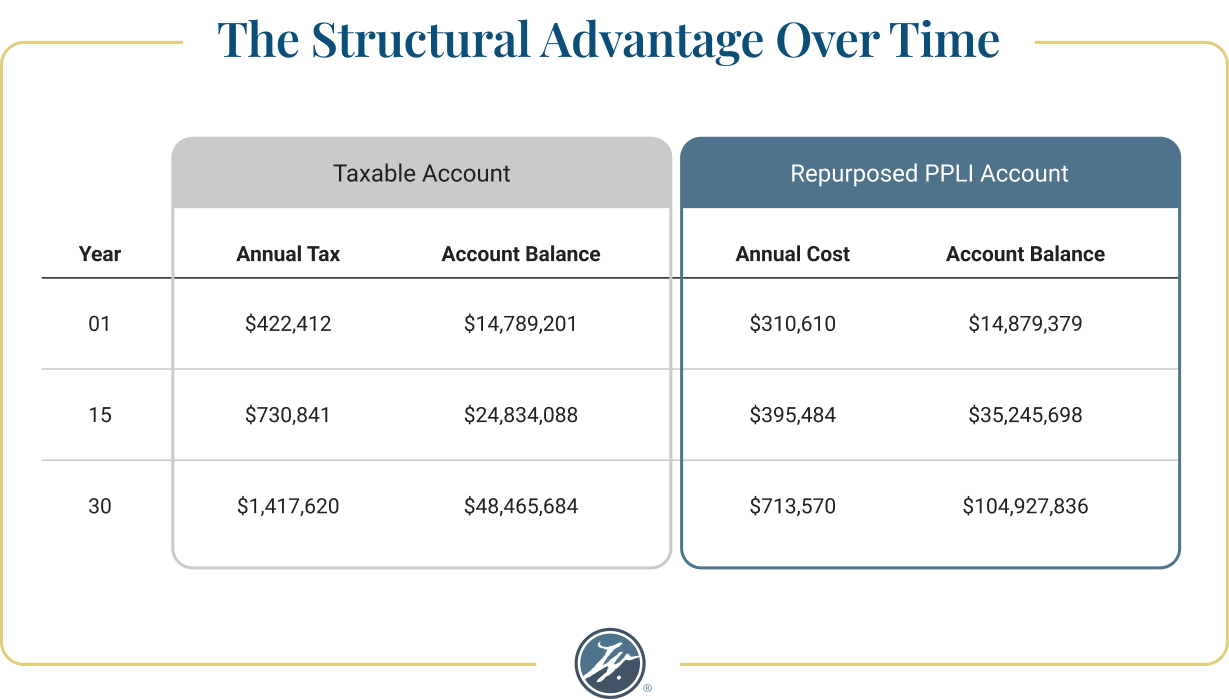

The Long-Term Impact: Repurposed vs. Status Quo

The comparison in the PDF shows the power of structural efficiency over three time horizons: Year 1, Year 15, and Year 30.

New PPLI Policy

- Year 1 Total Death Benefit: $32,688,877

- Year 15 Total Death Benefit: $54,918,870

- Year 30 Total Death Benefit: $125,357,337

The investment account grows from approximately $12.7 million in Year 1 to over $105 million by Year 30, while the original $20 million death benefit remains intact.

Status Quo (Taxable Account + Existing Death Benefit)

- Year 1 Total Death Benefit: $32,650,400

- Year 15 Total Death Benefit: $46,486,613

- Year 30 Total Death Benefit: $78,461,722

Under identical investment assumptions, the difference is structural. The taxable account erodes value through ongoing taxation, while the PPLI structure allows growth to compound tax-deferred. By Year 30, the modeled difference in total death benefit exceeds $46 million.

The investments themselves are the same. The tax structure is not.

Understanding the Cost Structure

One of the most important considerations in any insurance strategy is cost.

Repurposed PPLI is designed to be efficient

- No additional material cost of insurance. Existing policy costs are already accounted for or paid up

- Initial premium fees: Approximately 1.5%, including federal and state premium taxes

- Ongoing mortality and expense fees: Approximately 45 basis points

- Total all-in amortized lifetime costs: Approximately 40–45 basis points

The underlying principle is straightforward. When the long-term cost of insurance is lower than the taxes a taxable portfolio would otherwise incur, structural efficiency becomes a meaningful advantage.

The PDF summarizes it clearly: work with a trusted insurance professional to keep your existing insurance and add a tax-free PPLI account for less than 50 basis points all-in cost.

What Repurposed PPLI Protects Against

Over long time horizons, one of the largest drags on compounding is not volatility—it is taxation.

In the hypothetical illustration, the only variable difference between the two structures is tax treatment. Both scenarios assume the same 8% return. Both begin with the same death benefit. The divergence emerges from how investment growth is treated year after year. The taxable structure steadily reduces what remains invested. The PPLI structure allows assets to grow tax-deferred and be accessed tax-free.

Over decades, that difference compounds.

Simplicity in Execution

Another advantage is implementation efficiency. Traditional PPLI policies often require medical underwriting, exams, and lengthy documentation. Repurposed PPLI removes that barrier. No medical underwriting means:

- No exam

- No medical records

- No delay typically associated with new PPLI products

For clients already insured, this streamlines execution dramatically. The original death benefit remains fully intact. The structure simply adds a new tax-advantaged investment component alongside it. It enhances without disrupting.

Important Considerations

As outlined in the disclosure section:

- The financial data provided are hypothetical and intended solely for discussion purposes.

- Actual performance will vary and is not guaranteed.

- Variable life insurance products contain fees and may include surrender periods and additional rider costs.

- Investment options are subject to market risk, including loss of principal.

- This material is informational and not legal or tax advice.

These considerations are essential when evaluating any advanced insurance structure.

Is Repurposed PPLI the Right Fit?

Repurposed PPLI is most relevant for individuals who:

- Already maintain a significant permanent life insurance policy

- Seek greater tax efficiency

- Want to preserve their original estate planning structure

- Prefer minimal underwriting disruption

- Value long-term structural compounding advantages

It is not about replacing what works. It is about making it work harder.

The structure maintains investment growth potential, minimizes tax friction, and delivers both the investment account and the death benefit tax free to beneficiaries. For families focused on durability rather than short-term positioning, structural efficiency matters.

A Smarter Way to Leverage What You Already Have

Financial strategies evolve, tax exposure changes, capital grows; but thoughtful planning does not require starting over.

Repurposed PPLI provides a way to preserve existing life insurance while layering in tax-advantaged investment growth—without additional medical underwriting and without sacrificing the original death benefit. In the long run, structure matters.

And sometimes the smartest move is not replacing what you built—but refining it.