A Time for Reflection: Discovering Hidden Value in Life Insurance

Published: June 12, 2026

Most advisory teams know life insurance is rarely a “set it and forget it” asset. Needs shift, premiums climb, estate plans evolve; by the time a client wants out, the instinct is to surrender, lapse, or reduce. Each of those moves is permanent. Most of them quietly hand the value back to the carrier.

This WP90X session was built to interrupt that instinct.

Ryan Brusca of Coventry joined WealthPoint’s Vince Brunoforte and Ryan Barradas around a single idea: the full story is worth hearing before a client makes any irreversible move. The carrier’s number is rarely the best one available, and once that decision is made, it can’t be undone.

The Big Takeaway

If you only take one thing from the replay, take this:

A life settlement is rarely the headline solution. But it belongs in every policy review conversation, because surrendering, lapsing, reducing, or letting a term policy lapse are all permanent, and the carrier’s offer is rarely the best outcome on the table.

This is not a replacement for good planning, but rather a pressure test on it. The plan keeps its original purpose; the client simply sees every option before anything becomes final.

Start With the Screen: “Is There Real Value Here?”

One reason settlements get dismissed is the Partial Presumption that only a narrow set of policies qualify. The session made the opposite point. Term and universal life, especially the underfunded universal life facing rising premiums, are exactly what this market was built on, and shifting needs surface across nearly every policy a client holds.

The constraint isn’t policy type. It’s the profile. Before anyone talks offers, you pressure-test the fundamentals. Age and life expectancy come first: 65-plus is the sweet spot, and under 70 generally needs a health change to drive value. Face amount matters next, since larger policies are stronger candidates; Coventry’s average purchase runs around $2.5 million, with no upper limit. Then there’s funding reality, where an underfunded universal life policy staring down a premium increase is often the strongest candidate of all.

This is where the credibility comes from. The message isn’t “anything sells.” It’s “more qualifies than you think, when the screening discipline is real.”

Why This Changes the Game: It Catches Value Before It Disappears

Each year, roughly $150 billion of life insurance owned by seniors simply lapses or is surrendered. That value goes back to carriers, often because the subject was never raised. Conventional thinking treats an unwanted policy as a sunk cost.

The secondary market reframes it as an asset with a buyer. That unlocks two practical advantages. The first is optionality: clients facing premium fatigue or a looming term-conversion deadline gain a real alternative to walking away. The second is re-entry, since older or impaired insureds, often the hardest cases, are frequently the strongest candidates.

And none of it requires abandoning the original planning objective.

The Two Clarifications That Eliminate Most Objections

The most important “yes, but…” in the market is simple.

First, the client controls the outcome. They can take cash, or through a retained benefit they can keep a portion of the death benefit assigned to their own beneficiaries while shedding the premium entirely.

Second, the decision stays informed. WealthPoint models keeping the policy alongside selling it, so the family decides with the full picture in front of them rather than reacting to a single carrier figure. If a policy is a good enough investment for a fund, the honest question is whether it’s a good enough investment for the family to keep, and the family deserves to see both sides before choosing.

There’s nuance, since trust ownership, beneficiary alignment, and timing all matter, but the principle holds. This is about widening the client’s options, not forcing an exit.

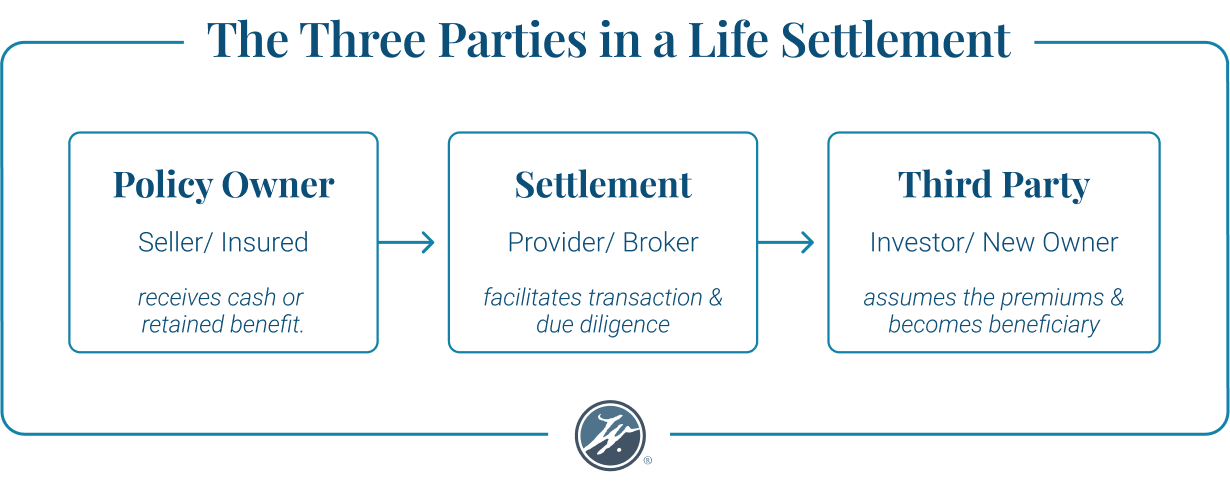

What a Life Settlement Actually Is (Without the Noise)

At its simplest, an existing policy is sold to a third-party investor who becomes the owner and beneficiary, takes over all future premiums, and ultimately collects the death benefit.

The value to the client shows up in the form they choose. It can be a lump-sum cash offer today, often well above cash surrender value. It can be a retained benefit, with no more premiums but a portion of coverage preserved for chosen beneficiaries. And it’s a clean 1099 transaction, thanks to the 2017 Tax Cuts and Jobs Act, which removed the old cost-basis reduction for insurance charges and put more money in the seller’s pocket.

This framing keeps it grounded:

This is often a decision change, not a coverage loss. Same insured. Different owner. A better outcome than a lapse.

The Enhanced Cash Value Program: A Fast Path for Healthy Insureds

One of the more useful advisor takeaways was a genuinely new development. Coventry’s enhanced cash value program purchases policies on healthy insureds with no medical underwriting, pricing off age and gender, then using an annuity to fund the premiums.

It isn’t health arbitrage. Made viable by today’s higher interest rates after a decade of lows, it opens the market to clients who’d never fit the traditional impairment model. Currently marketed for 65-plus, it’s a clear signal of how far this market has matured past where it sat a decade ago.

Cost, Framed Correctly

The broker fee is benchmarked three ways: one-third of value created, 20% of the gross offer, or 6% of face amount. WealthPoint averages the three and then applies a discount. In the case study below, that discipline returned roughly 9% more to the trust than the standard structure would have. The question isn’t “Is there a fee?” but this:

Is the net to the family meaningfully better than surrendering, lapsing, or reducing?

For the right policy, that trade becomes hard to ignore. And the question of fees, compensation, or conflicts is one WealthPoint expects clients and advisors to ask out loud.

When It Stops Being Conceptual: The Case Study

This case study uses a fact pattern we often see at WealthPoint. There were two identical policies on a single insured, both owned inside an irrevocable trust. The insured looked “too healthy” to sell, up at 4 a.m. for five-mile walks. And the grantor, after successful estate planning shifted assets to the next generation, could no longer comfortably afford the $234,000 a year in gifted premiums needed to carry the coverage.

The first annuity-based offer already beat the roughly $600,000 surrender value by about half a million dollars. But WealthPoint pushed further, with a call to the insured and then a full medical review, and surfaced significant impairments beneath the healthy lifestyle. Those findings lifted the gross offer to $1.94 million.

The story wasn’t a lucky break. It was discovery done properly. The family weighed selling one policy to fund the other, selling both, and surrendering, then chose to sell both, take the certainty, and enjoy that wealth together while dad was alive, rather than betting on a timeline.

What the Q&A Confirmed: Durable When Serviced

This discussion reinforces something important: this strategy isn’t casual. It requires process.

Themes include trust alignment and ownership structure, policy health and durability, carrier differences and retained-risk requirements, the timing sensitivity of offers as treasuries and annuity rates move, and the discipline to say “this isn’t a fit” when it isn’t.

The takeaway is that the value is earned through diligence and honest screening, not the elegance of the concept.

Who This Is For

This tends to be most relevant when a client owns meaningful coverage they no longer want or need, when a term policy is nearing its conversion deadline and won’t be fully converted, when the insured is 65-plus, older, or impaired, when you’re conducting an ILIT or estate plan review, when premium fatigue is setting in, or when the policy screen comes back strong.

If you’re reviewing policies or ILITs this year, a settlement analysis is a natural pressure test. It isn’t a default recommendation, but it’s a conversation worth having when the raw material is already there.

The Better Sequence: Hear the Story Before You Surrender

Before any permanent decision, confirm the insured’s age and profile fit the market. Validate the policy’s face amount and funding reality. Compare the settlement value, both cash and retained benefit, against surrendering, lapsing, or reducing. And run the fact pattern by WealthPoint while the option is still open.

When those disciplines are in place, a life settlement can be one of the cleanest ways to recover value an existing plan was about to give away. When they aren’t, it shouldn’t move forward.

A Closing Thought

Many clients are about to hand a valuable asset back to the carrier through a surrender, a lapse, or a reduction they can never reverse.

A life settlement asks a narrower question:

Before that decision becomes permanent, has anyone checked whether the market would pay more?

For the right clients, the answer changes everything. The key is asking before the door closes. If you have a fact pattern in front of you right now, that’s the conversation to start with WealthPoint.