Modeling PPLI Accumulation: Asset Location, Not Asset Allocation

Published: March 4, 2026

When taxes rise, long-term wealth outcomes are shaped not just by what families invest in, but where those assets live. Asset location—the choice of account or structure holding investments—has become a key factor in whether capital compounds or erodes over time.

For families planning across generations, the question shifts from “How do we grow wealth?” to “How do we preserve compounding wealth over decades?”

One solution increasingly used is Private Placement Life Insurance (PPLI): a privately structured life insurance policy for sophisticated investors that allows assets to grow tax-efficiently while supporting long-term estate planning.

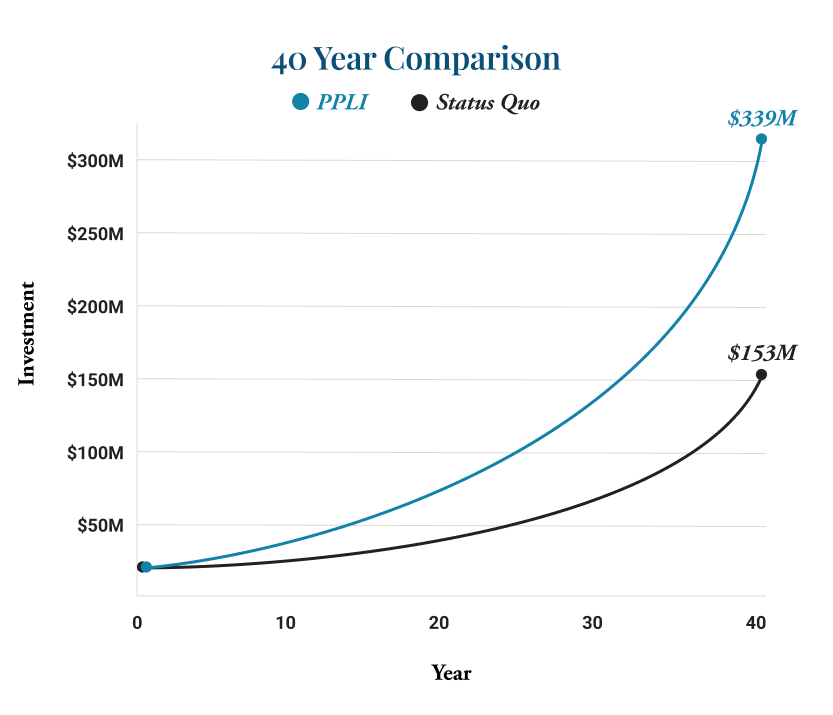

WealthPoint’s Ben Rainey walks through the accumulation model below, showing how a $20M allocation grows to $329M net-to-heirs with PPLI versus $134M in a taxable account—using identical investments.

PPLI: A Shift in Location, Not Strategy

Over long time horizons, family capital outcomes are driven more by asset location than by asset allocation. PPLI adds a new tax-efficient “location” to the balance sheet without disrupting investment strategy, advisor relationships, or portfolio philosophy.

Assets remain with the same trusted advisors, managed under the same allocations and governance standards. The only change is the structure holding those positions. By relocating assets into a tax-efficient environment, PPLI reduces ongoing tax drag while preserving portfolio integrity.

The Tax Drag Conundrum

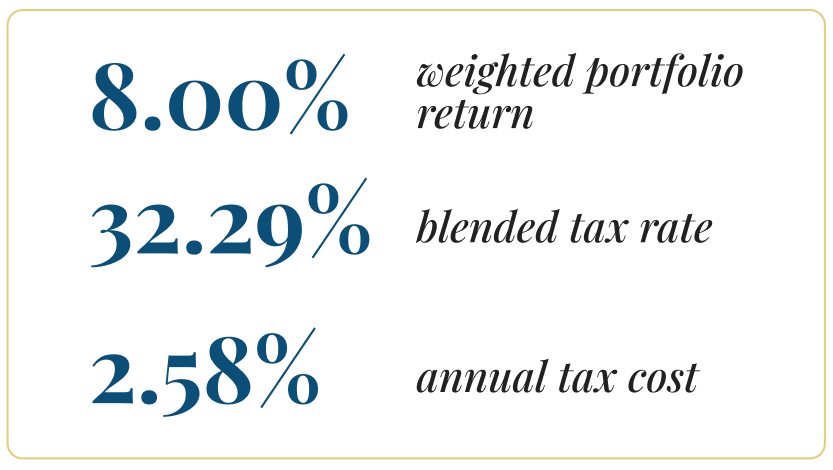

Most investors focus on gross returns, often underestimating how annual taxes compound over decades. Even modest yearly taxes erode long-term performance.

Our model uses these assumptions:

That 2.58% recurs every year. Over decades, it becomes a structural drag. Over a 40-year period, even seemingly small annual taxes meaningfully reduce final outcomes.

Relocation, Not Reallocation

Inside a PPLI structure, nothing changes about how the portfolio is built or managed. The same advisor team oversees the same allocations, using the same investment process, philosophy, and governance standards.

In practice, an investor might hold an identical five-fund allocation in both a taxable brokerage account and a PPLI policy—same positions, same weights, same risk profile. The only difference is where those assets live and therefore the structural costs associated with the location. By relocating capital into a tax-efficient structure, families preserve portfolio integrity while improving long-term compounding. Risk, return expectations, and oversight remain constant; the annual tax drag does not.

By relocating assets into a tax-efficient structure, families preserve portfolio integrity while improving compounding efficiency. Risk, return, and governance remain constant. The only change is the annual tax drag.

Status Quo vs. PPLI at Year Forty

A $20 million investment grows to $153 million in a taxable account over 40 years. The same investment in a PPLI structure grows to $329 million net-to-heirs—a $195 million difference driven entirely by eliminating annual tax drag.

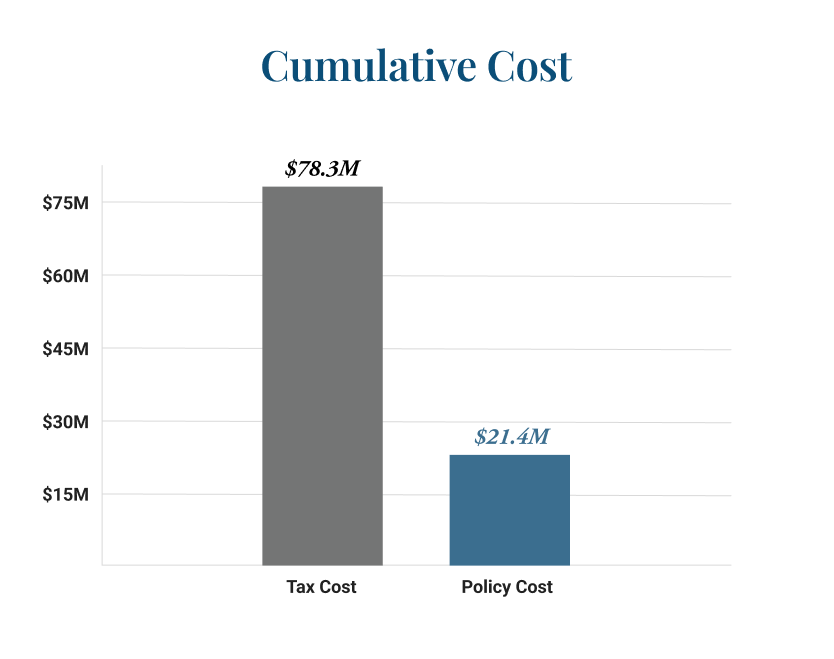

The taxable account pays $78.3 million in cumulative taxes. The PPLI policy incurs $21.4 million in insurance costs. The $56.8 million in net savings compounds into the $195 million outcome difference above.

Why PPLI Works

No structure is free, and PPLI is no different. PPLI includes several charges and expenses over the life of the policy. However, over long accumulation periods, these costs are typically far lower than the cumulative taxes incurred in a comparable taxable portfolio. What’s more, the PPLI cost structure is known and durable compared to the ever changing income tax rates.

The long-term advantage isn’t complexity or structure—it’s uninterrupted compounding. When assets grow without annual tax drag, more capital stays invested, and the compounding effect accelerates year after year, driving generational outcomes.

Funding with Intention & Death Benefit Design

PPLI works best when it’s funded thoughtfully. In our model, premiums are contributed over three to four years, totaling $20 million, which allows the structure to settle into place without unnecessary strain. One of the most important design elements is how to most efficiently contribute the desired premiums while maintaining the lowest possible death benefit required by the IRS. WealthPoint works with the owner and his or her team to minimize the death benefit to what’s actually needed to support legacy objectives.

This approach reduces ongoing insurance costs, keeps more capital inside the policy where it can continue compounding, and ensures the structure stays aligned with long-term planning goals. In our model, the initial $80 million death benefit is intentionally reduced after the premium period to minimize long-term drag. The focus isn’t on maximum coverage—it’s on efficiency and durability over time.

Key Considerations for Maintaining Tax Efficiency

To preserve PPLI’s tax benefits, policies must follow strict IRS guidelines that determine whether the structure works as intended.

- Investor control rules: The underlying account must be fully discretionary and a 3rd party advisor must manage all trades. Clients cannot direct specific investments, which protects the tax-advantaged status. (This does not apply if the client wants to self select certain Insurance Dedicated Funds (IDFs) as those already meet the Investor Control rules.)

- Diversification requirements: Portfolios must meet §817(h) standards to prevent over-concentration in any single asset.

- Funding rules: Policies must be funded with cash, not transferred securities, to avoid triggering taxable events and violating Investor Control issues.

- Underwriting: Unless the client has existing life insurance that can be used for PPLI, full medical underwriting is required. PPLI is life insurance, and the insurance company needs to assess risk.

- Early-year performance: PPLI often lags taxable accounts initially due to policy charges, but the compounding advantage emerges quickly, often by the 2nd or 3rd year.

These rules ensure the structure delivers tax-efficient compounding over decades.

The WealthPoint Approach

WealthPoint approaches PPLI with a single priority: preserving long-term compounding through disciplined structure and ongoing oversight. When designed intentionally and managed over time, PPLI functions as another account on the balance sheet, one built to reduce tax drag without disrupting strategy, advisors, or governance.

Contact us to model your specific situation and explore whether PPLI fits your family’s strategy.