PPLI vs. PPVA: Understanding the Key Differences

Published: December 18, 2025

When sophisticated advisors mention tax-efficient investment vehicles, two acronyms frequently surface: PPLI and PPVA.

Both are private placement insurance structures designed for qualified purchasers.

But they solve different problems for ultra-affluent families.

In this article, we’ll break down what sets them apart and help you understand which might align with your family’s objectives.

Similarities between PPLI and PPVA

PPLI (Private Placement Life Insurance) and PPVA (Private Placement Variable Annuity) share several characteristics.

Both require $5 million in net worth to qualify and follow strict investor control rules. Additional similarities include:

Transparent costs

No surrender charges

Deferred income taxes

No K-1s

But here’s what’s most appealing to both strategies: your assets stay at your current financial institution. You continue working with the investment team you’ve already chosen and trusted. We collaborate with your existing advisors rather than replacing them.

In addition, both solutions work with the full spectrum of investments your advisors recommend, whether they’re traditional securities, hedge funds, private equity, real estate, or other alternative strategies.

Differences between PPLI and PPVA

While these approaches share common features, they solve different problems.

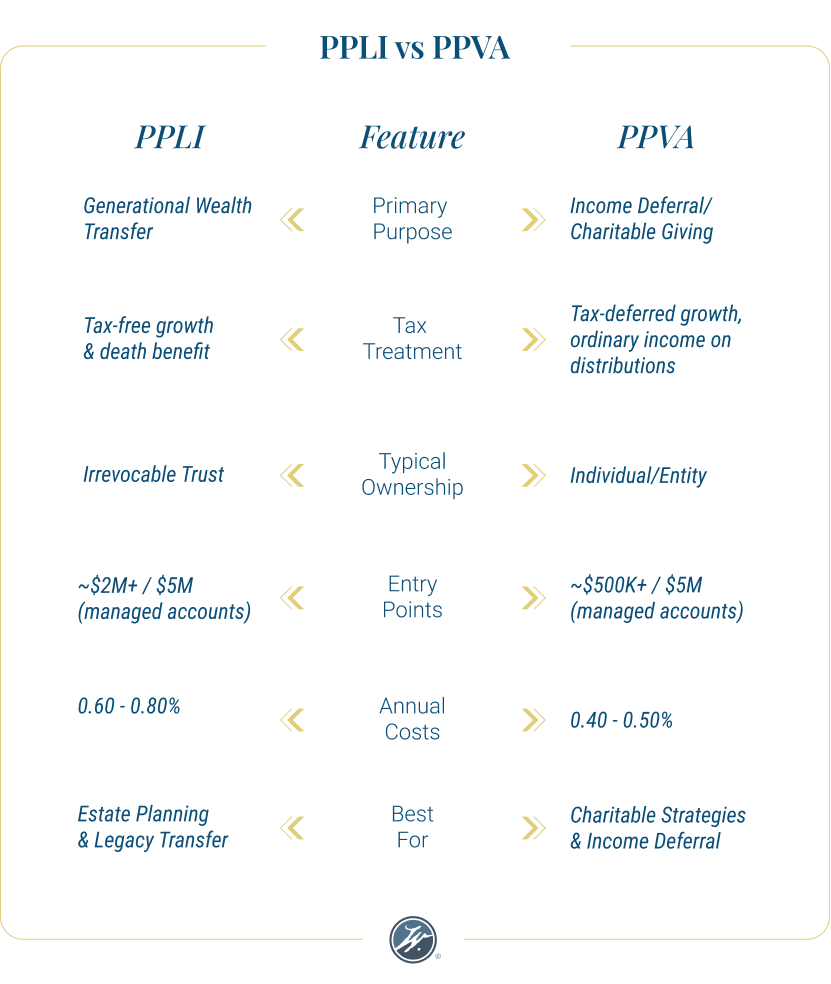

PPLI acts to move wealth tax-efficiently to the next generation. But, PPVA functions more like a sophisticated deferral mechanism, often used when charitable giving or income timing are priorities.

Tax treatment shows where PPLI and PPVA truly differ, however.

PPLI provides tax-free access during your lifetime and delivers a tax-free death benefit to heirs. PPVA offers the same tax-deferred growth, but distributions during your lifetime face ordinary income tax rates. At death, unless assets transfer to charity, your beneficiaries pay ordinary income tax on all growth.

Ownership structures reflect these different purposes. PPLI often sits in irrevocable trusts, creating a valuable step-up in basis for heirs. PPVA is typically held under individual or entity ownership, which offers more flexibility for charitable strategies.

There are also cost differences between the two structures. PPLI typically costs 0.60-0.80% annually while PPVA runs 0.40-0.50%.

This chart illustrates the main differences between PPLI and PPVA.

How to Decide What’s Best for You

The choice between PPLI and PPVA comes down to understanding your family’s priorities and timeline. While both offer compelling tax advantages, each serves distinctly different planning objectives.

Are you prioritizing wealth transfer to heirs or optimizing for charitable giving and income deferral? Some families benefit from both approaches for different objectives. Others find one clearly superior for their circumstances.

In our experience, the most successful outcomes happen when families avoid a few common missteps:

Don’t expect immediate benefits – both strategies work best over longer time horizons.

Adequate funding is crucial; insufficient capital can undermine the advantages you’re seeking.

Remember that liquidity operates differently than traditional accounts.

Proper design matters more than fees alone. The lowest-cost option rarely proves the best fit for your unique circumstances.

Your existing advisory team knows your situation best. If you’re exploring which approach might serve your goals, we collaborate with your current advisors to evaluate fit.