Want Drama? Don’t Prepare for Estate Taxes

By Tim Young & Michael Kenneth

There’s something out there. Something looming.

You can’t quite put your finger on it. But the air around you cools as its shadow rises over your shoulders and the sun fades slowly away.

It feels maybe like a rogue wave at sea. You don’t know exactly when it’s going to hit. But if you sail enough and you don’t prepare, it rises from nowhere and swallows you whole.

Or 40 percent of you, at least.

If you’re a successful business owner, that looming specter is estate tax. Ignore it at your peril.

Is that too melodramatic? Too sensational? If you think so, consider this real-life drama.

Every day in our country, the heirs of personal estates that include successful, privately owned businesses they have inherited are challenged with producing millions of dollars—fast, within nine months—for the purpose of paying estate tax.

Every day. No drama.

Very much like a rogue wave, the federal estate tax—40% of an estate’s taxable value—wipes out or nearly wipes out the business. In some cases, it’s a liquidation. In others, it’s a quick sale. In yet others, it’s a loan to pay the tax using the business as collateral that creates crippling cash flow problems from having to repay principal and interest.

The effects of unplanned for estate tax are real. And so is the drama they can cause.

The state of estate tax

Federal tax law dictates that any individual with a net worth over a certain amount is subject to estate tax. This exemption amount changes annually based on the rate of inflation. For 2023, the amount for an individual is $12.92 million. For married couples, it’s $25.84 million.

This means that the estate of an individual who passes away in 2023 with a net worth higher than the exemption amount will owe a tax of 40% on the difference between their taxable net worth and $12.92 million. Depending on their state of residence, they may owe even more in state estate taxes.

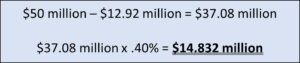

For example, an individual with a taxable estate of $50 million dollars will be assessed an estate tax of about $14.8 million. Here’s the quick math:

This situation worsens in 2026 when the exemption amount will be cut by about half. The current amount resulted from a doubling of the exemption under the Tax Cuts and Jobs Act in 2018. It’s set to expire in 2026, unless extended by law.

Using the same example as above and factoring in current tax law (keeping in mind that even if extended, the 2026 exemption amount could be higher or lower than 2023), the $14.8 million bill increases to about $17.4 million, simply because someone passed away in 2026 instead of today.

Now that the start of Q4 2023 is just days away—and given the potential complexity of planning and analysis—2026 is much closer than it seems.

Excuse me, I’m going to need another $2.6 million, please?!?!?!

Issues for generational businesses

Estate tax issues are especially worrisome for generational businesses.

If you had a great business—$50 million, $150 million or even higher in value—and you monetized it, your heirs bite the bullet and pay the tax because they have the resources.

However, if you have a generational business that you want to pass on to your heirs, there is no monetization event. They likely don’t have the $50 million to buy your shares. You don’t even want them to have to buy your shares. So, the compounding effect of estate taxes—having to be paid on top of taxes on annual earnings—can create serious issues.

And the higher the net worth, the worse the problem gets.

Estate tax assessment: How it works

The triggering event for estate taxes, of course, is a death. After the death, heirs are required to file an estate tax return, which effectively notifies the government of the death and the taxable event.

An estate tax return requires disclosure of the decedent’s assets, including any businesses or business interests, as well as their fair market value. Depending on the nature of the assets—for examples, art, jewelry and especially a business—an independent assessment of fair market value may be necessary.

Business valuations are typically conducted by independent appraisers that have experience in evaluating not just business assets, but also less tangible factors such as volatility of earnings, as well as lack of marketability discounts, minority ownership and non-voting discounts, risk discounts and others.

Heirs have nine months from the date of the death to file the return and pay the tax.

Mind-set: Estate tax is a subjective tax

At the end of the day, it’s all about planning and looking at estate taxes subjectively: Without proper planning, you—thinking on behalf of your heirs—elect to pay the tax. However, if you do the proper planning, you can minimize or mitigate the tax and its effect on your heirs.

There are many options: converting your business to liquid assets, life insurance policies to provide liquidity to pay for the tax, estate planning or estate freezing techniques, charitable planning and other options.

It’s subjective. It’s a choice. And the choice begins with planning. Now.

###